This article originally appeared on www.thesavvycouple.com and was re-published here with permission.

(graphic created by Becky Neubauer for TheSavvyCouple)

Have you thought to yourself, “How much should I save each month?” but never found a satisfying answer? There are different ways to approach this question, and it can be overwhelming to decide the right amount to set aside.

Don’t worry, we’ve found the best answer to your question and will show you exactly how much money you should save and how to save it! Personal finance can be confusing, but we are here to simplify your journey to financial freedom.

If you’re looking for a rule of thumb, try saving 20% of your monthly income. This is a good starting point and can be adjusted depending on your financial situation. You may need to save more or less depending on your circumstances, but this will give you an idea of where to start.

Let’s dive into how to calculate the amount of money you should be saving each month and how to find the money to set aside. We’ll also discuss how to set aside emergency savings and retirement funds to achieve your financial goals!

How Much Should I Save Each Month

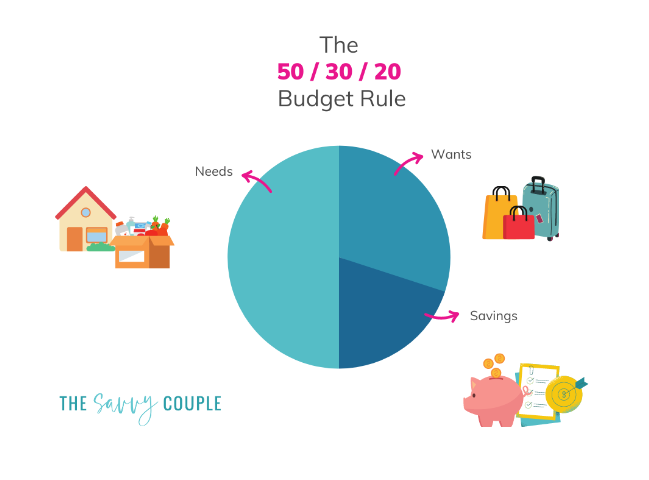

50/30/20 Rule

If you’re wondering how much money you should save every month, here is a handy rule to follow. To calculate how much money to set aside, you should know your income. Then calculate your take-home pay or after-tax income.

When it comes to your income, you should put 50% towards necessities, 30% towards discretionary spending, and 20% towards savings and paying off debt. This is also a good rule of thumb for beginners who are saving money or learning how much to save each month.

Think of your necessities as the absolute basics that you need to survive, such as groceries and rent. Discretionary spending on fun stuff covers the rest of your living expenses like clothes and going out to eat.

You should put the last 20% in savings for later use. This way, you can set aside money towards a vacation or other major purchase without feeling like you’re depriving yourself to save.

You have to keep in mind that these numbers are adjustable and not set in stone. While a 20% savings rate is a good rule of thumb, you should feel free to move the percentages around to suit your needs.

Why save 20%?

To break it down, if you make $50,000 a year after taxes and other deductions, 20% of your income works out to be about $10,000. That’s over $800 that you’ll save each month to put a hefty five-figures in your savings account or investments each year.

It’s essential to build up emergency savings so you can easily handle any unexpected expenses. Also, by starting to invest and saving for retirement now, it will be much easier to achieve financial freedom.

In general, putting 20% of your income away for your future goals and purchasing assets is a great idea. These assets could include rental homes, retirement accounts, stocks, mutual funds, bonds, and more.

How To Save Money

Saving money doesn’t have to be complicated or difficult. Make saving part of your routine because building saving habits will improve your financial future. Set up automatic transfers from your checking account into savings so that the process is automatic and easy to stick with over time.

Determine Savings Goals

The first step to financial independence is to figure out how much to save each month. It is about setting savings goals with a planned end date in mind.

Why are you saving money? What do you want the money for? Is it a new car? A family vacation? Have a plan and then work backward from that point to determine how much you need to put aside each month to reach your goal by your deadline.

Debt repayment plays a significant factor in determining how much you can afford to save. The more money you have available after paying off all your debt, the more you will be able to put away for savings each month.

If you are struggling with debt repayment, prioritize that before you start saving. In Dave Ramsey’s baby steps, he recommends saving $1000 for an emergency fund and then focusing on paying off all debt. After you are debt-free, you can go back to saving.

Short-Term Goals

While it’s good to have a long-term savings plan, you should also put some money aside for more immediate expenses. It may be new tires for your car or that one big bill that comes due every month.

If you want to save for a vacation or other major expense, you can save about one-third of the total budget each month so you have the cash on hand before you need to spend it. Having short-term goals will give you a sense of accomplishment as your savings grow.

The most important part of saving is putting it in a place where you can access it easily when needed. Don’t put your savings into an account with high fees or penalties for withdrawals if they are needed before you expected to use them. Instead, open a checking or savings account that allows you to withdraw quickly and easily.

Long-Term

Many people are good savers when it comes to the short term, like a vacation they are looking forward to, but they struggle when it comes to saving for other purposes like retirement or future home purchases.

However, long-term savings should be a priority too. If you have a child going off to college in the future, start putting money away now so that you can help them pay for it without having to take out student loans (or go into debt yourself).

Long-term goals may also include investment plans to build your net worth or other goals that have a much longer time horizon like saving for the closing costs of your dream house.

It’s best to invest long term savings so you can take advantage of the compound interest and growth from the stock market over time.

Prioritize Your Emergency Fund

Your emergency fund should be your first priority when it comes to saving. According to CNN Money, 4 out of 10 Americans say they can’t cover a $400 unexpected expense.

That means that an even more significant portion of the population does not have an emergency fund that would cover three months or more if they lost their income or had another significant financial setback.

Six months’ worth of expenses is a good target savings goal. This way, you will be prepared if unexpected expenses arise.

After completing your emergency fund goal, continue to put cash away for retirement and other long-term savings goals.

Don’t Forget Retirement Savings

It’s important to consider retirement planning far before you reach retirement age. This may sound daunting to you, but you can start saving for retirement even if you just set aside a hundred dollars each month.

Your 401(k) or Roth IRA should be first on the list if you want to take advantage of the tax benefits these retirement accounts offer. Be sure to contribute at least enough to get your employer match, which is free money you would otherwise be leaving on the table.

Get started investing for retirement today with Betterment.

Create A Budget

Budgeting is essential to your financial health. While creating one can feel like a hassle, it’s definitely worth it when you see how much easier it is to save money when you know your spending habits.

This is especially true if you want to allocate 20% of your income to your monthly savings and limit overspending on unnecessary things. These are some of the tools that will help you create a budgeting plan that works.

Mint

Mint is an excellent resource for finding out where your monthly income is going and how to make the most of every dollar you earn. Just connect it to your financial institutions, and it will automatically track your spending for you.

Mint will even send you alerts in case you’re spending more than usual in certain categories, like groceries. If that happens, check out our tips for saving money on groceries!

Personal Capital

Another great tool to use when it comes to setting a budget and figuring out how much you can really start saving each month is Personal Capital. This website lets you know what percentage of your income you’re spending on housing, transportation, or entertainment and how close you are to your monthly savings goal.

Since it shows you exactly where your income goes based on your spending habits, you can make sure you’re living within your means. This app will also suggest how much you should save each month to reach your investing goals for retirement.

Get A High-Yield Online Savings Account

The best place to put short-term savings is in a high-yield savings account. CIT Bank (member FDIC) is a great option for a savings account.

You should aim for 6 months worth of expenses for your emergency savings goal. This will be easiest to save by setting up automatic transfers from your checking account to your savings account on a regular basis each month.

A high yield savings account is also a great place to save for things like a down payment, home repairs, or holiday gifts. It’s better to put these funds in a savings account rather than the stock market, so you don’t risk losing them right before you try to buy a house!

Join Cashback/Rewards Apps

If you’re looking for an easy way to save money, another great option is downloading cashback or rewards apps.

Ibotta

Using Ibotta, you can get cash back on things you already buy at the grocery store just by scanning your receipt. It’s an easy app-based way to access coupons and deals on the stuff you were already planning to buy.

Honey

Honey is an easy to install browser extension that saves you money when you shop online. It will automatically try to apply coupon codes at checkout so you can save as much money as possible.

Capital One Shopping

If you want to earn cashback when you buy things online, then check out Capital One’s Shopping. Shopping through their portal will make it easier for you to save money while doing your regular online shopping.

Rakuten

You can shop through the Rakuten website and earn a percentage back on online orders. They also have a browser extension that detects savings available on online purchases you have in your cart.

Automate Your Savings

Once you’ve started budgeting and earning cash back on things you already buy, it’s time to start automating your savings. This means that you should sign up for auto-transfers into your online savings account or your retirement account.

This will put your savings and retirement contributions away every single month without you having to spend time thinking about it. It is the easiest way to put money away for things you need to save for, such as a down payment for a house.

If you’re not sure how much you should save each month, start by setting up an auto-transfer of $50 or another small amount from your income. Auto-transfers are the easiest way to make sure that you’re getting ready for retirement and achieving your savings goals without having to think too hard about your finances.

Invest Wisely

Once you know how much money you’ll be stashing in your bank account each month, it’s time to invest some of your savings. Be smart about where you put your savings so that you can take advantage of compound interest from investments.

Investing is a really great way to make sure that you’re putting enough away for retirement, especially since retirement accounts like 401ks and IRAs come with tax benefits. If you’re not sure how to start, financial advisors can help you make financial decisions based on your annual income, expenses, taxes, and savings goal.

Taking advantage of the stock market is important because it will help you reach your financial goals for retirement savings much faster. The typical return (right now) for savings accounts is 0.5%, but the average annual return in the stock market is around 10%.

You’ll want to save short-term money in a savings account and long-term savings in a retirement account or brokerage account. There are many apps you can use to open investment accounts and invest your money in stocks or ETFs without any fees.

Robinhood

Robinhood is a great investing app that offers zero-fee trading. This means you can earn all of the returns without having to pay anything extra when you buy and sell stocks or ETFs.

Having this online investment platform is a great way to make sure that you’re on track for your savings goals, but it can also be overwhelming when you don’t know what stocks or investments to buy.

That’s why Robinhood offers a lot of resources to help you use their app. There are free stock quotes, along with the option to create custom price alerts that let you know when the market goes above or below certain prices that you set.

Get started investing with Robinhood today.

Earn More

Blogging

If you want to increase your savings with a side hustle that allows you to work from home, then blogging is your best bet. You can’t just start a blog and expect it to make you millions of dollars overnight, but if you put in extra time and effort up front, you’ll reap the benefits later on.

Plus, you can start blogging for free or with very little money by using platforms like BlueHost. Bluehost is the platform we recommend to kickstart your blog.

Blogging can be another source of income that will help you put more money away for savings.

Proofreading

Like blogging, you can earn money from a job that allows you to work from home by proofreading documents. If you have a strong command of the English language and an excellent eye for detail, then this is an incredibly flexible way to earn some extra cash on the side.

Learn how to become a proofreader with the free 76-minute workshop from Proofread Anywhere. You can earn around $15-20 per hour in this job which can help you to put more money into your savings account each month.

If you have an eye for grammar mistakes and want to work from home, proofreading is a great choice.

Freelance Writing

If you have a way with words, then you can increase your income as a freelance writer. There are so many outlets to write for online.

Learn how to become a well-paid freelance writer with Earn More Writing. This is a great way to have an extra $500 or $1,000 in your monthly budget for your savings goals!

The great thing about freelance writing gigs is that they’re flexible, which means you can write when you have extra time in the morning or on the weekends.

Bookkeeping

If you have experience managing finances, then you can easily transition into bookkeeping. As long as you know your way around QuickBooks and other accounting software, this is a great choice for earning some extra money on the side.

You can learn more about bookkeeping and how to make it a side hustle through Bookkeeper Launch. Bookkeeper Launch is an online program that teaches you the skills to become a bookkeeper and start your own virtual bookkeeping business.

Bookkeeping is a high-paying side hustle. By working this side job, you will earn more money, and you will be able to achieve your financial goals faster.

If you want to have another source of income, there are plenty of ways to make money online, so you don’t have to rely on your monthly income alone. Try these side hustles to save more money for your future.

Just Get Started

Starting small with these steps can help you work up to how much money you need to save each month. This way, you can feel confident as you start saving for your financial goals.

No matter what life throws you, you can start saving today and plan for the future. Having enough savings can really make a difference, and saving now can help you build the life that you want without worrying about money too much in your old age.

Final Thoughts

To gain financial independence, you need to save a percentage of your income. Saving money is one of the most important things you can do for your future.

The best way to achieve your long-term goals is by creating and implementing a financial plan. As long as you are committed to this plan, you are on your way towards a better financial future.

By automating your savings and investing in low-risk investments, you can make sure that you have a cushion for retirement or any other personal finance goals you may have. Paying off debt like student loans will also allow you to save more and improve your credit score.

Having an emergency fund is also one of the best things you can do for your peace of mind, so make sure you’re prioritizing emergency savings above all else. If you have all of your bases covered, then you won’t have to worry about emergencies or retirement anymore.

You can even make extra money to increase your savings so that you can reach your goals faster. There’s no excuse not to start saving today!