Wouldn’t it be great if someone would tell you exactly how to create a new budget – for your first time, for the new year, or when your old one just isn’t cutting it? That’s what this post is all about – six straightforward steps that will help you put together your best budget ever. After following these steps, your new budget will help you achieve your goals and live in alignment with your values. How? First, you’ll be shifting from a “budget” to a “spending plan.”

Spending Plan Background

A Spending Plan gives you a framework for how and where to spend your money in order to achieve your goals and live your life in alignment with your values.

Want some background on how to create a Spending Plan and how it’s different from a budget? Read the Spending Plan 101 post, which discusses:

- The top 2 reasons to create and follow a spending plan (one is definitely not what you think!);

- A step-by-step guide on how to make a personalized spending plan;

- Questions to ask yourself as you create your spending plan; and

- Tips and tricks for making a spending plan work for you.

1. Use a Template

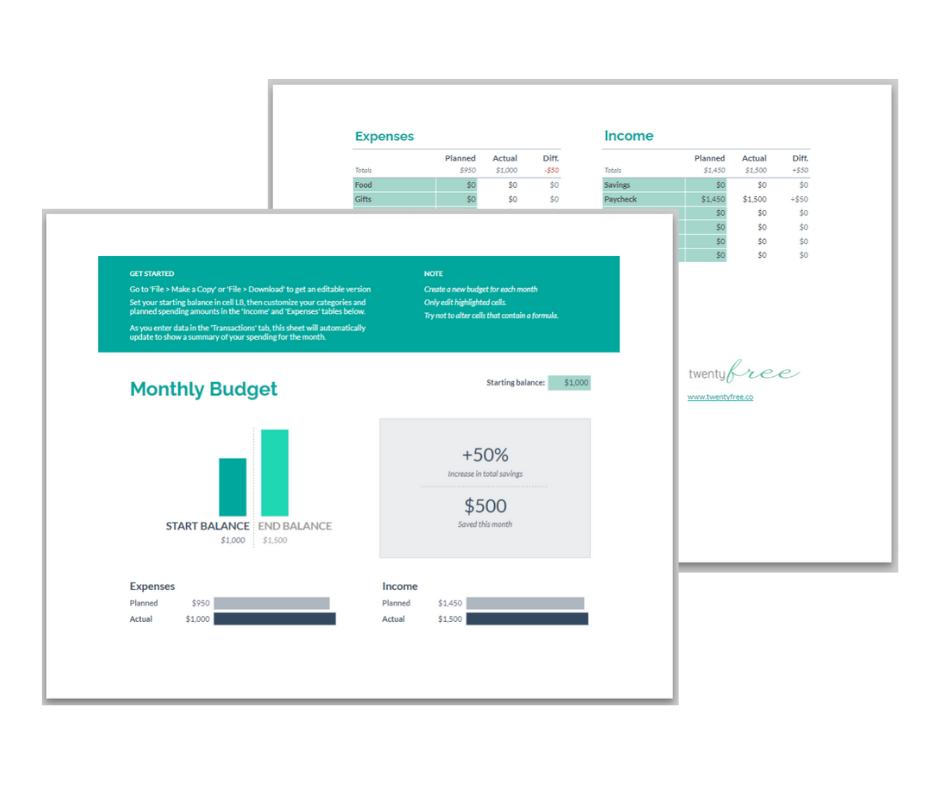

If you have an old budget, use the “Save As” function to make it a template for your new budget. No need to re-invent the wheel! You can tweak this all you want in the following steps, but it’s likely that the bones will stay the same.

Now if you have been using a traditional budget and not a spending plan, or if you’re new to budgeting, I’d recommend you download the Spending Plan Template to help you get started with this better way to budget. Remember, a spending plan intends to help you spend in alignment with your values.

2. Start With a Goal

The most important thing to decide when creating your spending plan for the new year is what your overarching financial goals are. Do you want to save an emergency fund? Start investing in your 401k? Max out your retirement accounts? Save for a downpayment on your first rental property? Pay off all of your student loans? All of the above (OK, tiger)? You get the idea. The sky is the limit.

This goal will inspire you to stick to your spending plan, and it will drive you to figure out more creative ways to cut expenses in areas that aren’t important to you while increasing your earnings and savings rate.

Build on your past goals

Look at last year’s goals. Think about how you can build on top of them. Some questions to ask yourself include:

- What did I achieve last year?

- What’s next?

- What is the most important thing for me to do financially this year?

Here’s some ideas based on my personal experience with setting goals. My driving goal in 2017 was to pay off all of my remaining high interest student loans. I actually achieved that goal and my goal for 2018 which was saving a 10k emergency fund, both in 2017. My new goal for 2018 was getting my net worth into the positive (even just $1!).

Set a Big Hairy Audacious Goal

A “Big Hairy Audacious Goal” (BHAG) is exactly what it sounds like – a BIG crazy goal. How do you set one of these? You take your new goal for this year, and you dream bigger. Don’t stop getting bigger and bigger until the goal is so scary that:

1. You don’t think you can achieve it in a year. If it’s totally realistic, you’re not shooting for the stars, and you’re not challenging yourself.

2. It’s so big you are a little embarrassed to admit it to other people. This fear is a great indicator that you’re getting out of your comfort zone. And that is so important for being able to achieve things you didn’t really think you could.

For an example of a BHAG, mine in 2018 is to not only have a positive net worth by the end of the year but to have over a +$50,000 saved/invested by the end of the year. I estimate that should land me at an approximate $15,000 net worth. This goal is $15,000 larger than my basic goal for the year! It’s a stretch goal that will drive me to go beyond what I was working towards and achieve even greater things. Even if I end the year with a $5,000 net worth, that’s $4,999 more than my original goal of having a $1 (positive) net worth!

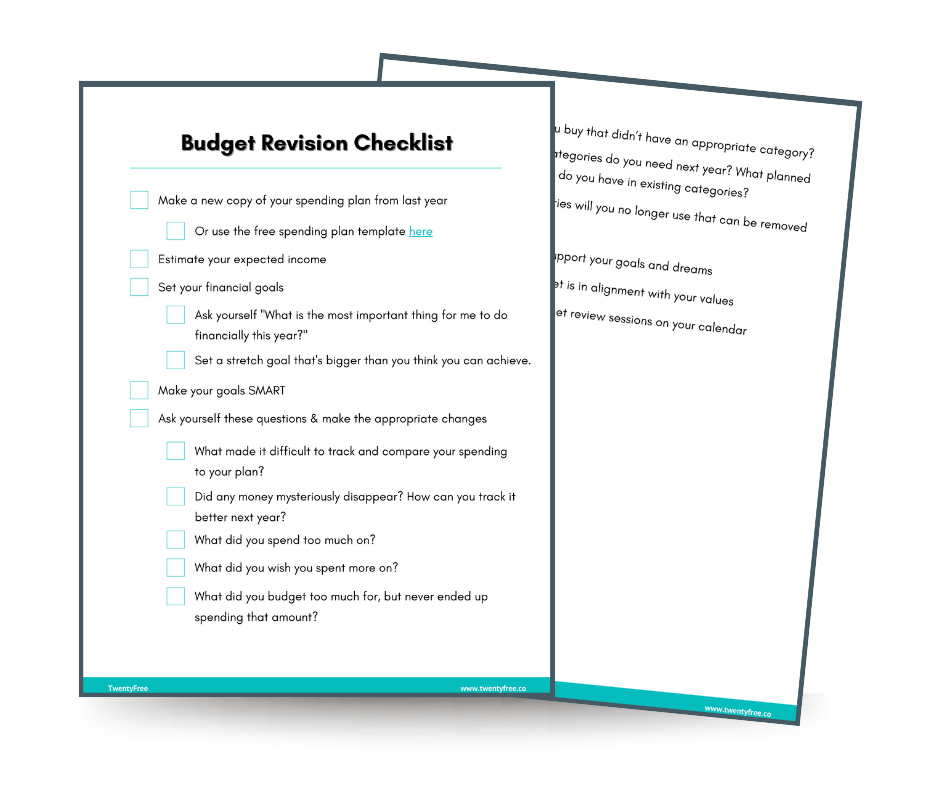

Make your goals SMART

When you are setting goals of any kind, the most effective way to set them is to make them S.M.A.R.T. This is an acronym that stands for Specific, Measurable, Achievable, Relevant, and Time Bound. This method of goal setting will make you much more likely to achieve your goals. Be sure to set a separate SMART goal for your basic goal and your BHAG.

- Read this article about setting SMART goals.

- Read this article about SMART goal templates.

3. Revise By Asking Specific Questions

I find it very useful to ask myself 8 questions that guide my revisions of my previous year’s budget. They are discussed in detail in this post: How to Simplify + Improve Your Budget in 8 Easy Steps.

Here are a few of the questions to ask yourself:

- What made it difficult to track and compare your spending to your plan?

- Did any money mysteriously disappear? How can you track it better next year?

- What did you spend too much on?

- What do you wish you spent more on?

The rest of the questions to ask yourself when revising your budget are available in the blog post or the downloadable checklist.

4. Align Your Plan with Your Values

You’ve already set financial goals in Step 2, and created budget categories for what you’d like to save, invest, or pay off. Now, revisit your personal goals for the year, and align your spending categories with these goals and values. This is important to do for both short-term and long-term goals. For each goal, determine if you will need to spend money on it, or if you could spend money on it in order to speed up your achievement of the goal. Then, create a budget category for each goal, and make a guess at how much money you would need to spend in order to achieve that goal (if short-term) or progress towards that goal (if long-term) in a year.

Having this money set aside gives you permission to spend it in support of your goals and dreams. This is a wonderful freedom to have, because you are setting out a plan ahead of time that will ensure your spending aligns with your vision of your best life.

For example, when I revisited my goals for the year, I added some categories and budgeted money specifically to achieve these personal goals, which reflect my personal values. In order to maintain my health through physical activity, I’ve planned to spend money on Sports; to encourage myself to pursue self-improvement, I’ve allocated $200 to spend on apps and journals and classes, etc; and to give myself permission to hire professionals to assist with my financial planning, I’ve planned to spend money to hire a CFP and/or CPA.

5. Look at Your Budget as a Whole

You’ve probably been updating your spending plan spreadsheet throughout this process. You may have added new categories, deleted old categories, increased or decreased budgeted amounts for certain categories, and switched things around.

Now’s the time that you zoom out and take a big picture view. What percentage of your budget is going towards your necessities (the big three: housing, transportation and food)? If you ordered your categories from largest (most money budgeted) to smallest (least money budgeted), would this be in direct alignment with the things you value most and the things you value least? If not, move some money around.

Also, it’s really important to forecast your income for the following year. I would recommend basing this projection on your past year’s income, and not inflating it by too much unless you are sure of the increased amount. You can always increase your budgets later once the new income is ensured, but it will be hard to get back the money you spent if that income never materializes. Make sure that overall, you haven’t budgeted more money than you expect to make next year.

6. Schedule Regular Maintenance + Review

If you don’t put this on your calendar, it might not happen. Decide the frequency with which you’d like to review your finances (weekly, monthly, or perhaps quarterly) and add it to your calendar. You could use a paper planner, a wall calendar, or an online calendar. If you add this to your online calendar, I’d recommend setting a reminder for one or two days in advance so you can start getting prepared before you do your review (and you won’t forget!).

When you perform your budget review, do regular maintenance. I’ve described a few guidelines about lessons I’ve learned during my budget reviews in this post about perfecting your budget. Tip #4 and #5 are probably most relevant to short-term reviews: give yourself time + freedom, and be honest with yourself.

Here’s how I do my regular reviews: On a monthly basis, I review my finances using a program called You Need a Budget (YNAB). That’s when I pay my bills, evaluate my spending according to my Spending Plan, tweak the Spending Plan for the coming month(s), and send any extra money to my investment account (previously, this was going to pay off my student loans). On a quarterly basis, I see how I am progressing towards my goals, and make sure my saving is on track. And on a yearly basis, I sit down and follow the steps above to create a new and improved spending plan that fits my goals and needs for the upcoming new year.

Quarterly Report Examples:

- Q1 2017 Financial Review – $2,072 of Student Loans Paid Off

- Q2 2017 Financial Review – $21,500 of Student Loans Paid Off

- Q3 2017 Financial Review – $4k of Student Loans Paid Off + $5k Emergency Fund Saved

- Q4 2017 Financial Review – I saved $11,400 in 3 months!

- 2017 Review – $27k Student Loans Paid Off + 17k Saved + $950 Spent Per Month

Yearly Spending Plan Examples:

- Spending Plan 2017 – Pay off $31.8k of Student Loans, Live on 850 per Month

- Spending Plan 2018 – Save $15k, Invest $24k, Live on $1k per Month

Bottom Line

Now is a great time to get back on track with your financial goals, and create a budget that sets you up for success. First, use your old budget as a basis for this new one. I’d recommend starting a Spending Plan if you haven’t already – we even have a Spending Plan template that you can download.

Write down your financial goals, and then do something crazy – make them bigger. Then, ask yourself specific questions that will help you adjust your budget and make it even better this year.

Next, align your plan with your values by creating budgeting categories that correspond to your personal goals as well as your financial goals. Then, take a step back and look at the big picture of your budget. Does it reflect your values and goals? Have you accurately projected your income? Finally, you need to make time on your calendar for regular review and maintenance sessions.

Your Turn:

What was the most significant change between your old budget and your new one? Please comment below!

WANT TO REMEMBER THIS? SAVE THESE TIPS TO YOUR FAVORITE BUDGETING PINTEREST BOARD!

This is great advice for people in their 20s. I wish I had access to such comprehensive information back then. Budgeting is the key to financial freedom. I hope people have a better grasp of its power after reading your article. Great work!

Thanks for your comment!

[…] Budget Cheat Sheet: How to Make a Brand New Budget in 6 Easy Steps […]

[…] Budget Cheat Sheet: How to Make a Brand New Budget in 6 Easy Steps […]

[…] Budget Cheat Sheet: How to Make a Brand New Budget in 6 Easy Steps […]

[…] Budget Cheat Sheet: How to Make a Brand New Budget in 6 Easy Steps […]

[…] best way to define financial literacy is knowing when to save and spend. It’s being able to create a budget and stick to it. It’s being able to assess financial opportunities and make sound investment […]