Did you graduate with a ton of student debt? I’ve been there. Here’s a step-by-step guide for new graduates who have student debt or anyone who wants to start paying off their student loans.

This article outlines the 10 crucial steps to pay off your student debt faster and reduce the overall amount your student loans will cost you. It is meant to help you comprehensively understand your options when it comes to lessening the long-term financial impact of your student debt, whether you owe $10,000 or $100,000.

Using these steps, I paid off $67,000 of my high-interest student loans in just two years and two months. This saved me $24,000 in interest.

Step 1: Celebrate your Graduation!

Graduating college is a major win for your financial future – be sure to celebrate it! Remember what you spent your loans on. Sure, you gained solid skills to exceed expectations at any job, but also knowledge you can’t learn in any classroom, experiences you couldn’t have had anywhere else, and a fancy piece of paper (aka your diploma) that will ultimately help you earn 82% more money than if you hadn’t graduated a 4-year college.

Furthermore, gratefulness has been linked to happiness. Being grateful for all of the experiences you had while in college – all of the inseparable friendships, impromptu games on the quad, and that one breakfast item the cafeteria was actually good at making – will make you happier post-graduation. And if you weren’t smiling so hard your face hurt at graduation, it might put a smile on your face to know that gratitude has also been shown to raise optimism levels and self-esteem, and people with a positive outlook and strong self-esteem have higher incomes. So gratefulness, in the end, could lead to higher earnings throughout your career.

Graduating from college with a bachelors degree will have a large, positive impact on your lifetime earnings, so don’t despair about the amount of money you spent acquiring your diploma.

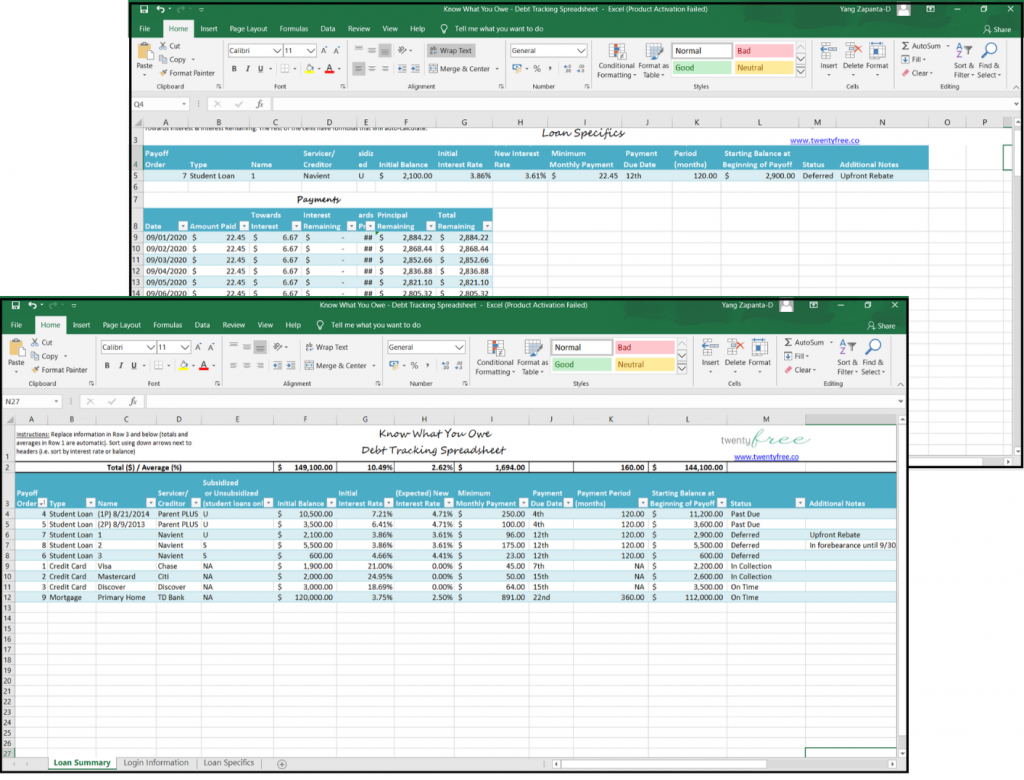

Step 2: Know What You Owe

This part is simple, but simple doesn’t always mean easy. Facing the numbers is a rough but necessary step towards becoming free from student debt. If you don’t know how much you borrowed, you’re not alone. According to one study that used nationally representative data, nearly half of students seriously underestimate the amount of student loan debt they have.

To take stock of what you owe, use the “Know What You Owe” spreadsheet to write out each loan’s type (such as Federal Stafford, Parent PLUS, etc.), if it was subsidized or unsubsidized, its initial balance, and its interest rate.

It is important to know both the amounts and the types of loans you have since this will affect your repayment strategy. This website is a one-stop-shop for finding all of your federal loan information. If you have private loans, you will need to log into your loan servicer’s website to get details.

Loan Types

Federal Stafford Loans

The federal government lends this money to eligible students in set, capped amounts each year. There are two different types of federal Stafford loans. One is government subsidized, and the other is unsubsidized.

Direct Subsidized Loans

The federal government pays the interest on this loan in a variety of situations – while you are in school, and while you are in your grace period, deferment, or forbearance.

Direct Unsubsidized Loans

The federal government does not pay interest on these loans. The interest will accrue from the day you take the loan until the day you pay it off.

A noteworthy feature of Stafford Loans is that the federal government offers different repayment programs that include payment plans based on your income, or even loan forgiveness based on public service.

Direct PLUS or Parent PLUS loans

Direct PLUS loans are often called Parent PLUS loans, which are federal student loans that are taken out by the parents of the college student. Direct PLUS loans can also be taken out by graduate or Ph.D. students. Ultimately, the parent or graduate student is the responsible party to repay the loan.

Federal loans, including Stafford and PLUS loans, are sometimes eligible for government forbearance, where payments may be temporarily put on hold by the federal government for a certain period of time, and they will also pause the interest. This is what happened in 2020 during the pandemic as part of the economic aid packages. As of the writing of this article, all federal student loans held by the Department of Education are in forbearance with suspended loan payments, a stop to collections on defaulted loans, and a 0% interest rate until December 31, 2020.

Private loans

Another financing option for college is to take out private loans, such as a personal loan from a bank. These would tend to have higher interest rates than federal loans, as well as less flexible repayment options.

Step 3: Pay accrued interest before it capitalizes

Interest accrues on some loans even while you attend college. This interest will capitalize at the end of your deferment period, which is typically the day you graduate. Save in order to pay off this interest before it capitalizes, because it can be thousands of dollars. Even better, pay it off as you attend college so it doesn’t have time to accrue into a large sum.

Capitalized interest will make your loan more expensive than the original amount you borrowed. This is because, at the time of capitalization, any unpaid interest will be added to the principal of the loan. Your loan’s principal amount is the amount you originally borrowed, which is what interest is calculated on.

Capitalized interest raises the amount of your loan, which will increase the amount of interest that you are charged and increase the total you end up paying for that loan.

Step 3.5: Pay accrued interest before it capitalizes… again!

The interest will capitalize again on your loans once your grace period expires. Find out when your grace period ends and repayment begins. This may vary if you have different servicers! You can either call your loan provider or check on their website.

You will want to make sure you know how to log in so you can be tracking your payments and progress on paying down your loans. In most cases, detailed repayment information will be mailed to you 20 to 60 days before payment is due.

Step 4: Get a job

Use that hard-earned diploma to earn yourself some money. Spend the time to find a job that you will actually enjoy while also compensating you well.

The book “What Color Is Your Parachute” by Richard Bolles can help you decide what field you want to work in and learn how to job search.

Step 5: Pay off what you can right away

Look at your savings and see what you can afford to pay off right away. Maybe you have some money saved from working over the summer, or there is a little extra in your bank account from Christmas gifts. Less interest can accrue when you make a payment ASAP.

Step 6: Refinance high-interest loans

Refinancing is basically taking out a new loan and then using that money to pay off the original loan or loans. The new loan should have better terms for this to make sense, such as a lower interest rate or a fixed interest rate rather than a variable interest rate.

Be aware that there are downsides to refinancing that include transaction costs or loss of benefits. For example, you will often pay 3% to 6% of the loan balance to refinance, and refinancing or consolidating federal student loans to a private loan means that you are no longer eligible for benefits such as deferment, forbearance, or loan forgiveness.

When you consider refinancing, make sure you read the fine print. Some bank loans will penalize you for paying them off early because they want all of that interest money. Additionally, keep in mind that longer loan terms, such as 10 years, often have lower interest rates than shorter loan terms, such as 2 to 5 years. Therefore, ensure that there is no early re-payment penalty, and go for the longer term while secretly planning to pay the loan off as quickly as possible.

If you decide to refinance your student loans, check out SoFi. This link will give you a $300 welcome bonus if you choose to refinance with SoFi. Again, please do your research and understand the new terms before refinancing any loans.

Step 7: Apply for Income Based Repayments on Direct Loans

This program is called different things by different servicers, but it is often available for direct government loans like subsidized and unsubsidized loans. In some cases, for the first three years (depending on your income) your subsidized loans won’t accrue interest.

You still may want to apply for this program even if you can afford your minimum payments. By decreasing the amount you pay for low-interest direct loans, you can increase your contributions to higher interest loans. Therefore, you will pay less interest overall.

When you get income-based repayments, they will never be higher than your regular minimum payment. The calculation compares your gross income and family size to the poverty level to determine your eligibility. If you’re eligible, your payment is usually around 10% or 15% of the difference between your income and the poverty level for your family size.

Income-based repayment is based on your initial loan amount, so if you pay off any loans, your minimum payment won’t increase. This means it can be a good strategy to apply for income-based repayments before you pay off any loans in full. Additionally, paying down your principal balance doesn’t reduce your minimum payment.

You’ll have to re-certify that your income is eligible for income-based repayments once a year. Therefore, you should apply for income-based repayments when your income is low, such as before you get a job or when you’re at an entry-level salary so that your payments will be reduced as much as possible.

Save money on interest by reducing your minimum payment for all of your loans, so you can focus on paying off high-interest loans first.

Step 8: Ask about how to reduce your interest rates

While you’re on the phone with your student loan servicer, make sure you ask them about any ways you can reduce your interest rate.

Most student loan servicers offer a discount for auto-paying your minimum payment. Ask how soon you can set up the auto pay and apply for the interest rate discount.

If you’re doing auto-pay, create a specific savings account for paying your student loans out of. Once you get a job, set up a direct deposit to this savings account. This deposit should be your minimum payment each month.

Save an amount that would cover 3 months of your minimum payments into this account as a buffer, so you know you’re covered for student loan payments for at least 3 months if you lose your income, and you will never overdraw your account. And, you can subtract 3 months of minimum payments from the final amount because you have it saved in your auto-pay account!

When you set up auto-pay, you can set a date for it to pull money from your account. If you’re auto-paying two different minimum payments, you can set them to pull money on the same day of the month to make tracking payments easier. You can also change the date to be after your paycheck direct deposits your payment amount into your Student Loans savings account.

Step 9: Make a plan to pay extra

Now that you’ve done everything you can to decrease your interest rates, you can focus on the best way to decrease the amount of interest you pay on your loans: paying them off faster.

Here are three ways to find extra money to pay extra towards your student loans.

1. Reduce Your Expenses

Look at your current expenses and see what you could stop spending money on for a little while so you can put that money towards your student loans. Could you take on a roommate to pay part of the rent, or cancel a subscription for a couple of months so you have more money to put towards your loans?

Related: 67 Ways To Reduce Your 3 Biggest Expenses: Housing, Food & Transportation

Additionally, focus on your discretionary spending. Ask yourself if spending money on those cocktails or that dress is moving you towards your goals, or if you’d be better served by putting that money towards your student loans. By implementing goals based spending, you’ll find it easier to spend in alignment with your goals without having to follow a restrictive budget.

Related: A Step-by-Step Guide to Using a Spending Plan To Achieve Your Goals

2. Defer Saving and Investing

While you’re working to pay off your high-interest student loans, hold off on saving for things like vacations or travel. You can also put off investing while you’re paying down your debt.

Invest enough to get your company 401k or 403b match, so you’re not leaving money on the table. Otherwise, you may want to wait to invest until you’ve tackled the high-interest portion of your loans.

It can be hard to decide whether to pay off debt or invest, or to do both at once.

The bottom line is that the return on investment of paying off high-interest student loans with an average interest rate of 7% is the same as 7% estimated market returns on stock investments. Therefore, your net worth will be affected equally by paying off high-interest student loans as by investing. On top of that, you get the peace of mind of getting rid of debt and reducing monthly debt payments!

3. Make More Money

There are plenty of ways to make more money. You can find a different job that pays more or ask for a raise at your current job. If you get paid overtime, you can work more. Or, start a side hustle or part-time job on nights and weekends. When you get paid extra, such as bonuses or tips, put that money directly towards your loans. You can even earn a little extra money using cash back rewards credit cards and by signing up for bank accounts that offer bonuses.

Related: Earn Extra Money: 9 Awesome Ideas You Can Use This Week

Step 10: Revise your plan often to pay off your debt earlier

Based on changing circumstances, such as getting an extra job, a raise, or a bonus, or figuring out a way to decrease your expenses, you may be able to revise your plan. The more you put into your loans now means less interest is going to the bank.

Put a meeting on your calendar once a month to re-evaluate how much you can put towards your student loans that month, based on increased income and decreased expenses.

Conclusion

There are 10 steps to pay off your student debt faster and save thousands in interest. First, celebrate your graduation, know what you owe, pay accrued interest before it capitalizes, get a job, and pay off what you can right away. Then refinance your high-interest loans, apply for income-based repayments, ask about how to reduce your interest rates, make a plan to pay extra, and finally revise your plan often to pay off your debt even earlier!

Now that you have a couple of ideas for how to pay extra towards your student loans, you can use that information to see how quickly you’ll be done paying them!

Your turn:

What are some strategies you have used to pay down debt quickly? Have you ever tried anything on this list? Comment below!

Related Content

[smart_track_player url=”http://traffic.libsyn.com/findyourfreedom/Episode_1_-_Becky_Introduction_FINAL.mp3″ social_linkedin=”true” social_pinterest=”true” social_email=”true” twitter_username=”fyf_podcast” ]

[fusebox_track_player url=”https://dts.podtrac.com/redirect.mp3/traffic.libsyn.com/secure/findyourfreedom/023-3.mp3″ twitter_username=”fyf_podcast” ]

[fusebox_track_player url=”https://dts.podtrac.com/redirect.mp3/traffic.libsyn.com/secure/findyourfreedom/25-320debt20payoff.mp3″ twitter_username=”fyf_podcast” ]

[smart_track_player url=”https://dts.podtrac.com/redirect.mp3/traffic.libsyn.com/secure/findyourfreedom/039-2.mp3″ twitter_username=”fyf_podcast” ]

WANT TO REMEMBER THIS? SAVE THESE TIPS TO YOUR FAVORITE STUDENT LOAN PINTEREST BOARD!