In this post, I’ll discuss the strategies I used to:

- Pay off $27,600 of student loans this year;

- Save a $10,000 emergency fund in 4 months;

- Increase my net worth by $40,000 this year;

- Live on less than $1,000 a month, while traveling and enjoying life; and

- Save $6,900 for investing in 2 months.

In 2017, I truly put my money where my mouth was and spent in accordance with my values and goals. This was the first year that I put a Spending Plan in place to give myself permission to spend on the things that mattered most to me, including the “enjoying life” category that included all things travel, learning, exploring, and experiencing new things, as well as my category for sumptuous food and well-crafted beer (aka food & alcohol).

I lived on an average of $950 a month, and still traveled to 12 states, visited a myriad of microbreweries and biergartens, attended various festivals, spent time at the beach and in the waves, built a raised bed garden that delivered fresh veggies all summer long, and got my motorcycle and boat licenses. Some things I chose to not pay for, though, include significant rent (I live with my partner at his family’s house in exchange for home improvement), a car payment (I drive a 14 year old car), new technologies (I made my 7-year-old computer “like new” for under $100 bucks), a cable bill (we don’t watch TV or netflix/hulu), or fancy clothes/gadgets/other stuff (I’m happy with what I have).

Saving money and paying down student debt is hard, and takes a lot of work. But you can do it without feeling deprived.

You just have to live and spend in accordance with your values. This year, I paid off $27,680 in student loans, and that includes the remaining balance of $56,000 of refinanced, high-interest loans. I also saved a $10,000 emergency fund, and put away almost $7,000 for investing. All the while, I enjoyed myself and my life, and made the most of being 24 years old! I reached these goals by sticking to my Spending Plan (well, sort of – see below), being clear on my objectives and values, and making extra money. In 2017, I earned an additional $7,645. Read below for the breakdown of how I did it all.

Spending Plan Review

(2017)

The first number shown is the yearly allocation for the category, and the 2017 – $ amount shows how much was spent total in 2017. In parentheses, the percentage spent of the yearly allocation is shown.

(Read this post for an introduction to spending plans)

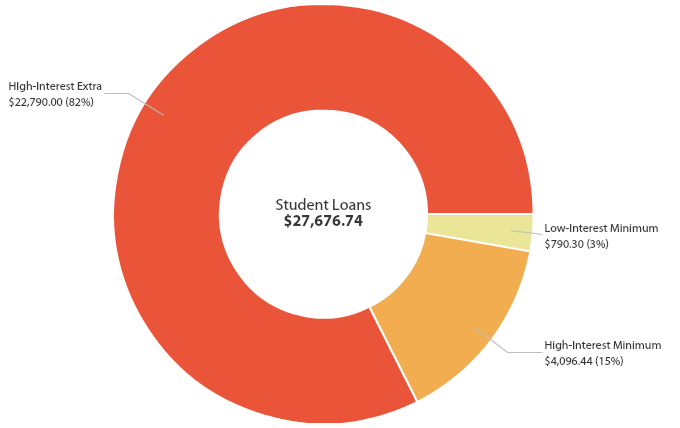

Student Loans

Low-Interest Minimum Payment – $790: 2017 – $790 (100%)

High-Interest Minimum Payment – $7,025: 2017 – $4,095 (58%)

High-Interest Extra Payment – $24,000: 2017 – $22,790 (95%)

Rather than paying off my low-interest loans once I made my last payment to the high-interest loans, I decided to save an emergency fund, and then save money for investing. This way, I start investing earlier, which helps me in the long run (thanks compounding interest!), and I will get important tax benefits from some of my investment accounts. I will also get a better return on investment (ROI) when investing rather than paying off my student loans. Stock investments in a low-cost index fund can be expected to return about 7% on average. That is nearly double the ROI that I receive when I pay off my low-interest student loans, which are sitting at interest rates of 3.4% to 4.6%.

Student Loan Payments – $31,815: 2017 – $27,675 (87%)

Savings Goals

Emergency Fund – $10,000: 2017 – $10,000 (100%)

Investing: 2017 – $6,900

I actually didn’t have a goal for investing this year since I didn’t think that I would have my high-interest student loans paid off until September, or that I would have my $10,000 emergency fund saved until December or January. Since I reached my goals early, in July and November respectively, I was able to set aside money for investing in November ($2,500) and December ($4,400) this year.

I still need to develop an investment plan for this money, so it has not been placed in any accounts yet. I have until tax day in April 2018 to make contributions to some of my tax-deferred accounts for the 2017 tax year, which will save me money on my 2017 taxes. I intend to consult with a professional before I make any moves.

I’ve also saved over $3,000 this year in my 401k from contributions deducted directly from my paychecks, as well as my employer match (this is not included in the $6,900 total).

Total Savings – $10,000: Q3 – $16,900 (169%)

Expenses

Enjoying Life – $2325: 2017 – $1,835 (79%)

Considering that I felt like I spent as much as I wanted on amazing experiences, I’m surprised I only spent 79% of the allocated amount in this category. Part of this can be attributed to the fact that I did not return to my boxing gym in the fall/winter due to my crazy schedule. Yes, all sport related activities (boxing, frisbee, etc) are considered “enjoying life” because I find them fun and life-enhancing.

The lesson learned here is that I don’t need that much money to have fun. After six or so years of living like a college student, living frugally seems a bit second-nature. I’ve come to realize that so many things I enjoy doing are free – going for a bike ride or walk, visiting the beach, playing cards with friends, enjoying conversation, hiking and enjoying the views. In 2018, I think I will decrease the allocation to this category in my Spending Plan.

Food & Alcohol – $2,220: 2017 – $2,900 (132%)

I love food, and I always look forward to a well crafted beer, so I’m willing to spend some good money on this category. Not that I’m above drinking Bud Light or anything (believe me, I drink plenty of it), but I won’t limit myself to cheaper beers just to save money. However, I do try to limit the frequency that I go out to drink, as frequent beers at the bar can add up quickly. This year I spent an average of $50 a month on alcohol, which doesn’t surprise me since I did do a brew tour of the United States in October, and went out with friends often throughout the year.

I don’t eat out much, but since cost-per-meal is so much higher at restaurants than at home, I spent an average of $50 a month on dining out. We almost always cook at home, which I enjoy because it is a hobby and good bonding time with my partner. It’s also healthier, and often easier than finding something I like on a menu, since I’m a pretty picky eater. We eat mostly vegan at home, which cuts out the most expensive grocery item – meat. Aldi, the best discount grocer in my opinion (and they don’t pay me to say that!), is where we shop for 90% of our food. I have tried, I mean really tried, to spend more than $150 there in one trip. Even with a full-to-the-top cart of groceries, it doesn’t seem to be possible! On average, I spent $135 per month on groceries.

The main reason I think I overspent in this category is because my Spending Plan allocations were too low. When I looked at my average grocery spending for the year, I was spending $135 per month, but only had allowed myself $120. I also spent double on dining and alcohol than I had anticipated. The numbers were simply too low! I reviewed the USDA Cost of Food chart, on which the government bases the food stamp program. In 2017, and it turns out that a monthly “thrifty budget” for a family of 2 is $382.70 ($191.35 per individual) and a monthly “low cost” budget for a family of 2 is $490.60 ($245.30 per individual). Rather than spending at my anticipated level of $185 per month (“thrifty”), I spent about $240 per month (“low cost”).

Since I get so much enjoyment out of food and drink, I consider it part of enjoying my life. To spend according to my values, and according to reality, so that I don’t start to feel deprived, I will adjust my 2018 food and alcohol allocation to continue spending around the “low cost” level.

Business – $225: 2017 – $215 (96%)

My spending in this category was essentially what I had expected. I had anticipated the costs for web hosting, domain, and my yearly Evernote and Crashplan (online backup) subscriptions. However, the amount of time I spent towards building my business was minimal, and far less than I had planned. I resolve to do much better in 2018.

Automotive – $2,930: 2017 – $2,075 (71%)

I am extremely lucky – a lot of my automotive costs (i.e. fuel, tolls, maintenance) were covered by reimbursements for the mileage I drive for work. Since I drive around a lot, my company reimburses me at the IRS rate for each mile in order to cover my work-related fuel and maintenance costs due to wear and tear. Since my car is in good shape for being 14 years old, and gets mediocre gas mileage (around 20 mpg average), I don’t accrue higher costs than the reimbursements. I was able to use the reimbursed fuel money to cover the gas costs for my personal travel, and the reimbursed maintenance money was able to cover the maintenance work my car needed including a set of new tires. This is the main reason I spent only 71% of the allocated amount in this category.

As I’ve mentioned before, I save a lot of money in this category by doing all the maintenance myself. Or rather, my partner does most of the hard work (he’s a mechanic among other things), and I help (and learn) and do the easier stuff myself. Instead of laying out $700 for labor related to replacing my spark plugs and wires, we spent a whole day and did it ourselves. I don’t pay for oil changes either, because I can do it in the time it would take me to drive to and from the shop, and it costs half the price. When we take long car trips, we always use my partner’s car, which is a 2001 Honda Civic he’s modified to be more aerodynamic. We average 40 miles per gallon (2x better gas mileage than my car) and split the gas cost.

Rent – $1,200: 2017 – $425 (35%)

Home improvement investment and labor is the rent my partner and I are paying for staying at his family’s house. We did a variety of projects this year such as tiling the backsplash in the kitchen, insulating half the house, completely overhauling the backyard, and building a raised bed garden. There are also small maintenance projects we do here-and-there to upkeep and improve the house.

Prior to living here with my partner, I lived at my parent’s house and paid no rent. Housing is relatively low on my list of priorities. Therefore, if I wasn’t able to have this inexpensive living arrangement, I would still be living with my parents in order to save as much money as possible.

Objects – $1,010: 2017 – $1,060 (105%)

Interestingly, I felt like I blew this category every month. I was surprised to find that I only overspent by about $50 for the whole year. Objects are low on my list of priorities because I find more value in experiences rather than objects. I am also an aspiring minimalist and live in a very small space (and plan to move into a tiny house!) so I don’t have the space or the desire to store many physical objects.

Spending in this category includes personal care items ($150), household items ($500 – double my goal), necessary clothing ($160), unnecessary clothing ($90), gadgets ($115), and gear ($50). I save money by getting most of my personal care and household items at either Aldi, Walmart, or Amazon. A good portion of the household items spending was gear for our household emergency kit, which set us back about $200. I made sure that at least 3/4 of the items in the kit would have regular use (either in our kitchen or in our camping gear), but there were some specialized items that needed to be purchased specifically for emergencies. Despite the expense, the peace of mind is worth it, especially since we live in an area that is prone to being affected by hurricanes and other natural disasters.

I also save money on clothes by not going to stores or malls, pretty much at all. I find I buy unnecessary things when I am just “looking” with nothing specific in mind. Regardless, I spent nearly $100 on clothing I deemed unnecessary, so I will be attempting to avoid stores even more next year. The only gear I bought was magazines for my airsoft gun (I got the gun as a hand-me-down from my cousin). Most gadget spending was on video equipment for the solar eclipse (which I will use for years to come), and a $9 hard drive enclosure for my old HDD. Last year I had bought a SSD for around $75 on black Friday, and finally got around to replacing it in my computer. So for less than $100 (and thanks to a free copy of windows 10), I made my 7 year old computer work like brand new!

Misc – TIAIC: 2017 – $2,465

The vast majority of spending in this category was related to health expenses ($1,995). Many of these expenses were incurred last year during my 2-week hospital stay, and a few were routine expenses such as contact lenses, prescriptions, and co-pays.

I spent $415 on gifts, about double what I had planned. I intended to get my Christmas holiday shopping done during the sales in January and February, and I did for about 95% off. What I didn’t anticipate was attending 3 weddings this year, or other smaller holidays such as Mother’s day. Next year, my partner and I have agreed that we are not giving each other gifts for any holidays (though that doesn’t rule out “just because” gifts), and instead we will just spend quality time together. My family has had this rule since I was a teen, so no pressure there, I usually just give handmade cards to let my family know I am thinking about them.

Losses – TIAIC: 2017 – $225

I essentially lost track of what I spent $225 of cash on this year. To avoid this next year, I will try to pay for nearly everything using my credit card so I can track it better. Of course, I pay every credit card bill on-time and in-full each and every month. If I need to divvy something up with friends, I’ll use Paypal or Venmo, which also have tracking.

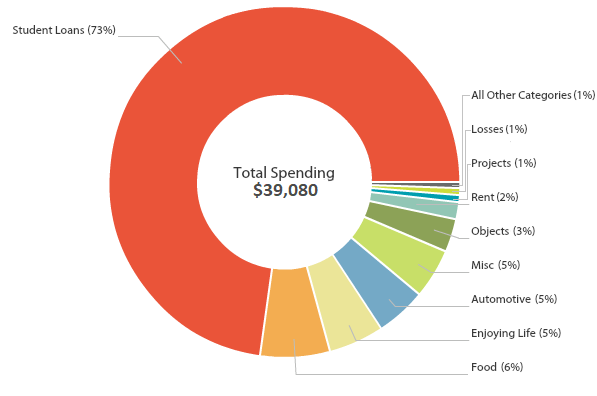

Total Expenses – $10,165: 2017 – $11,405 (112%)

Total Expenses + Student Loans – $41,980: 2017 – $39,080 (93%)

Total Expenses + Student Loans + Savings – $51,980: 2017 – $55,980 (108%)

Stats

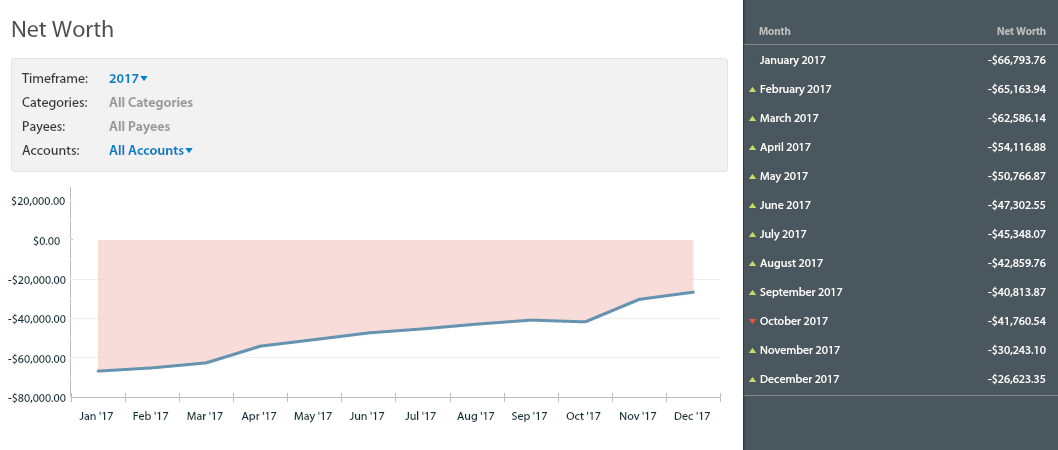

Net Worth

September 2015: -$102,800

January 2017: -$66,800

December 2017: -$26,600

Change in 2017: +$40,200

Change from 2015: +$76,200

*Doesn’t include 401k

Extra Income

Additional Full-Time Income: $4,840 – Although I got a raise in March and it was applied to my pay in April, I am not counting this as additional income. The additional income I am counting is net income from working overtime (I get paid my normal hourly rate for each overtime hour). Additionally, this sum includes my holiday bonus. With all the travel I did for work for a huge project with a tight deadline, I ended up working 60-70 hour weeks for almost 2 months. Throughout the year, I worked more than 6 additional weeks in overtime!

I do want to note that despite the extra earnings, working so much took a serious toll on my work-life balance. 12+ hour days (6 days a week) leave little time for anything else, and I was basically just working and sleeping in mid-September through mid-November. I am incredibly lucky to have a supportive partner – at the time he had a flexible work schedule, which meant he could cook and clean and pick up my slack while I was at work all the time. If I didn’t have him, I suspect my health (I had no time to prepare food, but he cooked almost every night) would have taken a serious hit. However, this wasn’t all rainbows and sunshine either. I was overworked, stressed out, and generally irritable, even towards the person who was helping me most. This certainly took a bit of a toll on our relationship, but we got through it.

Lesson learned – some amounts of stress and time-commitment are not worth the money. I didn’t have a choice of whether or not to do this project, but it taught me the value of my time and my mental serenity. In the end, I am so grateful that I was compensated for my extra time and effort, since the extra $5,000 was more than 2 months worth of extra payments for my high-interest student loans.

Tax Refund: $2,260 – This was far too high of a tax return amount, which indicated that my taxes were not properly anticipated and therefore too much money was withheld throughout the course of 2016. When I discovered this, I changed my W4 and state tax form to reflect more accurate withholdings so I will have a smaller tax return next year. The more money I get out of my paychecks up front, the faster I can pay off my student loans (and I’ll pay less interest too). Ideally, I will have a tax return of close to $0 next year, while not owing taxes.

Credit Card and Bank Rewards: $370 – I love credit card cashback bonuses, which are basically free money I earn for putting purchases on certain credit cards. I applied these cashback bonuses directly to my credit card bill (that I paid on-time and in-full each month), which freed up extra money to put towards my student loans and save for my emergency fund and investing. I also opened a bank account that gave me a $200 bonus! Even though I have since closed that account, the $200 was mine to keep!

Selling Items: $150 – I sold my college TV, since I don’t watch TV and it had been sitting in a box in my parent’s basement for the past 2 years. Easiest money ever.

Interest: $25 – I set up my student loan minimum payments to auto-debit from a high-interest savings account. I am also saving my emergency fund and investing capital in the same bank (each in earmarked accounts) with an interest rate of over 1%. This is much better than what I would have earned in a standards savings account, which typically offers something like .01% interest. I anticipate even higher earnings next year since my savings fund significantly increased in size at the end of the year.

Total Extra Income = $7,645

Investments

401k: All year, I’ve contributed the minimum to my 401k in order to gain the employer match. After all, this is the closest thing to a guaranteed return (aka free money) I’ll ever get! When I make additional income at my full-time job, my 401k contribution (which is a percentage) increases and so does the employer match. To date (including contributions prior to 2017) I have about $7,000 in my 401k, which includes my contribution, my employer match, and any losses or growth. For the majority of the year, this was the only investing that I was doing.

Now that I have $6,900 saved to invest, I really need to get an investment plan in place. Honestly, I knew that I’ve needed to do this for a while, and didn’t get around to it because I thought I had more time. I didn’t anticipate having extra money to invest this year. However, I crushed my goal of paying off my high-interest loans, so now that I only have the low-interest loans, it makes the most sense for me to begin investing, since I should be able to get returns that double that of my student loan interest rates. Stay tuned for my investment plan in the first quarter of 2018.

Final Thoughts

Hi there! Thanks for posting this!! I don’t have nearly as many expenses (no student loans, living with my parents, I take the train to work) like you do. Yet I am not able to save as much as you do. How do you do it?! It’s incredible and I love that you’re so detailed. I’ve been trying to work on a spending plan but I feel like I don’t have the knowledge to do it. For some reason I think excel is evil. Is your income pretty high?

Hi Wei, it sounds like you are at a really strong financial position right now, with no student loans or rent payment.

There are two main ways to save a lot of money – 1. Make more money and 2. Spend less money. I find it helpful to think of savings as a percentage of what you earn – a “Savings Rate” – because regardless of the amount of money you make, you can scale your savings amount appropriately. I personally aim for an 85% or higher savings rate, and by savings rate, I mean money I’m putting towards increasing my net worth. For someone who is new to saving, I would recommend setting a goal around 50% and then working up from there.

My base income is around the median for a college graduate ($50k/yr range), but as you can see in the Extra Income category, I do as much as I can to make more money by working more, selling stuff, etc. This year alone, I made an extra $7,500, all of which I was able to save (that’s 15% of a 50k/yr salary).

On the spending less money side of things, I think that really understanding where your money goes is the first step to spending less and saving more. And even though excel might seem evil, it is an useful tool for tracking your spending. If you want a more hands-off approach to start, I’d recommend linking your credit cards and accounts to mint.com, which will track your spending categories for you. Once you’ve done that for a month or two (maximum) you should have a good idea of where your money goes, and where you can start to cut back your spending. This is now the time to set up a spending plan, and explicitly set your spending and saving goals.

I actually have a Spending Plan spreadsheet that I am planning to share to my email list that will be coming out soon. If you are interested in getting this spreadsheet, you can sign up with the SUBSCRIBE link at the top of the page.

I hope that helps. Let me know if you have any more questions!

-Becky

[…] in student loans, saved $17,000, and limited my expenses to $950 per month (you can read the full breakdown here). These were amazing financial accomplishments that were fully aligned with my financial and […]

[…] 2017 Review – $27k Student Loans Paid Off + 17k Saved + $950 Spent Per Month […]

[…] I was spending was too much. This left too much wiggle room in the spending plan for my taste. My final spending amounts helped me decide on hard numbers for my previously TIAIC […]

[…] Latest Progress Report: 2017 Review – $27k Student Loans Paid Off + $17k Saved + $950 Spent Per Month […]