In 2016, my expenses were less than $4,500, but I still had a lot of fun – after all, my main priority is enjoying my twenties while aggressively paying off my student loans. I went to a few festivals, including a brew festival, a music festival, and a chowder festival (who knew that was a thing?). I also went waterskiing, won 2nd place in a 5k race, played in a few ultimate frisbee tournaments, hiked a portion of the Appalachian Trail, and flew in a small airplane. I explored a creepy abandoned psychiatric hospital (by myself!) and went camping with my friends. I also came down with a sudden debilitating illness that left me completely bedridden for two weeks and unable to work for a month. Thankfully, I was able to fully recover, though I am not looking forward to the hospital bills. There were also many, many beach trips, sunrises and sunsets.

Additionally, I made significant progress towards paying off my student loans. In 2016, I paid off over $33,000 of my student loan debt! That is 1/3 of my initial ~$100,000 debt! In 2015, I refinanced the high-interest portion of my student loans – approximately $56,000. In 2016, I paid off half of the refinanced loan! I focused solely on putting extra money towards the high-interest loan, and only paid the minimum payments on the low interest loans. My minimum payment for my low interest loans reduced significantly from $210 per month to around $50 per month because I entered an income based repayment plan.

I also quit my part-time job in August 2016 after working there for one year. I had received a generous raise at my full-time job and realized that I could increase my income faster by working more hours and working harder at my full-time job rather than splitting my focus between two jobs.

Another big development in my financial life this year… my partner and I opened a joint bank account just before the new year! Since we are now living together (oh yeah, I moved out of my parents’ house and into his parents’ house), we decided the easiest way to manage joint bills would be to pay into a joint bank account. This is a way for us to keep our personal finances separate while easily being able to handle our joint expenses. We have already had serious financial discussions about our future goals and ideal lifestyles and we are on the same page, so we had a strong basis to open a joint account together.

Spending Plan Review

(Read this post for an introduction to spending plans)

The first number shown is the (yearly allocation) for the category, and the 2016 – $ amount shows how much was spent 2016.

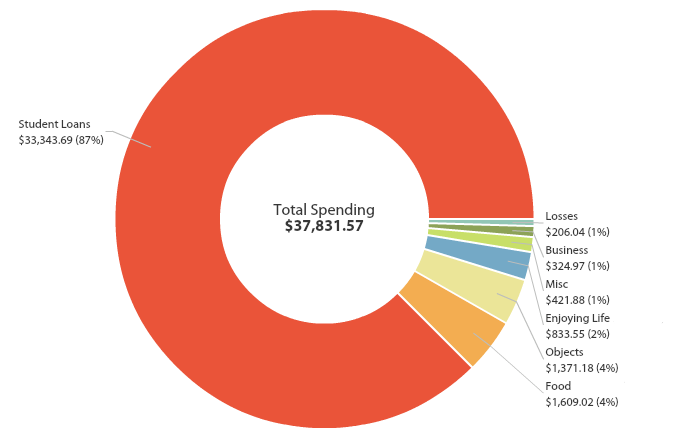

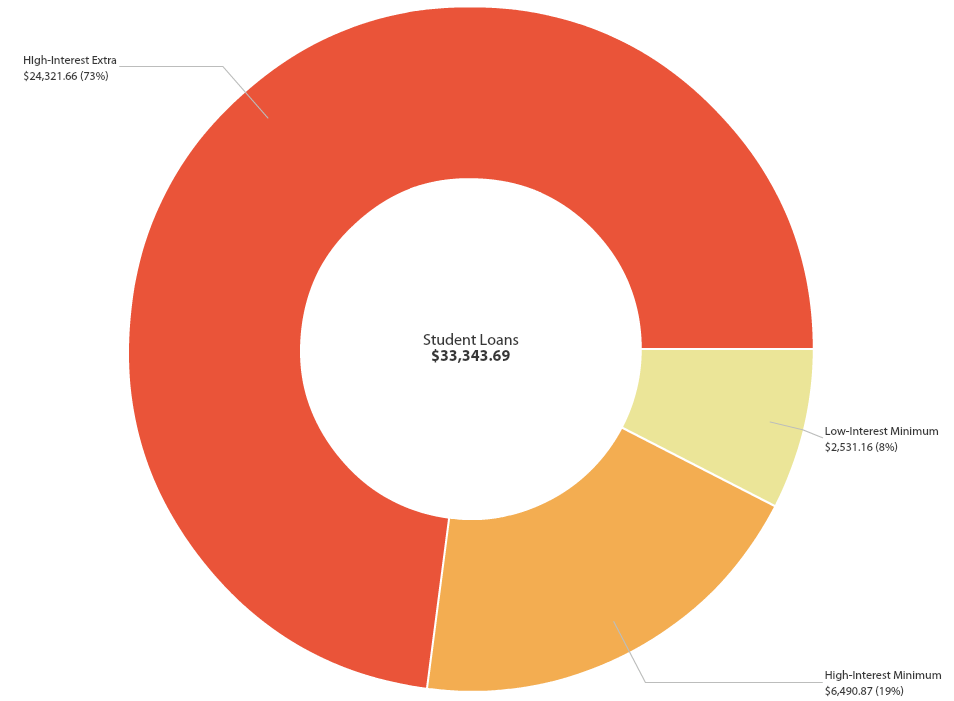

Student Loans

Low-Interest Minimum Payment ($2,530): 2016 – $2,530

High-Interest Minimum Payment ($7,025): 2016 – $7,025

High-Interest Extra Payment ($21,385): 2016 – $24,320

Using auto-debit, I paid exactly the budgeted amount to my student loan minimum payments. Then, I focused on using any extra money each month to make an additional payment to my refinanced high-interest loans. My initial goal was to pay $1,780 extra each month (I did a lot of calculating with my income and expected expenses and that was the hyper-specific number I came up with that I could afford in extra interest payments). I ended up using my savings and additional income to pay an extra payment of over $2,000 per month to my student loans!

Total Student Loan Payments ($30,945): 2016 – $33,345

Savings Goals

Travel ($5,000): 2016 – $0

In the beginning of the year, I decided that as part of my plan to enjoy my life and my twenties while aggressively paying down my student loans, I would save $5,000 for travel. I set up a direct deposit in the beginning of the year to automatically direct savings to a high-interest checking account specifically earmarked for this goal. I tossed around the idea of visiting Yellowstone for two weeks with one of my friends, but we never finalized plans and I had many opportunities to travel locally very cheaply throughout the year. So, I changed this savings goal to my housing contingency plan for once I lived on my own – a tiny house. See below.

Tiny House ($5,000): 2016 – $3,845

The travel savings accrued in my high-interest savings account totaled $4,150 in June. I re-named this account “Tiny House,” and continued my automatic deposits. However, in July, I decided that I had quite a while until I would need cash for a tiny house, so I used the $4,000 in the account for additional student loan payments. I continued contributing to this savings account via direct deposit, increasing them at one point to $700 per month, and ended the year at a strong $3,800.

Emergency Fund – On Hold

Throughout 2016 my emergency fund remained in its specified high-interest savings account, accruing a few dollars of interest. The savings goal is on hold until I pay off my high-interest student loans.

Total Savings ($5,000): 2016 – $3,845

Expenses

Enjoying Life ($960): 2016 – $835

I spent more than expected on sports this year since I started boxing again in December and the gym fee was quite high. However, we did not spend as much as expected on experiential dates, so I ended up doing quite well in this category.

Food & Alcohol ($2,160): 2016 – $1,610

This category was a good example of how flexibility is an important aspect of a spending plan. Food expenses were difficult to plan for because I didn’t know if or when I was going to move out of my parents’ house. I ended up moving out in October, and then over-adjusting the allocation to compensate for additional living expenses such as food. I didn’t have a realistic idea of how much food would cost each month, and I didn’t account for the fact that my partner and I were going to be splitting the expense, so food & alcohol spending this year came in well under target.

Business ($240): 2016 – $325

I overspent in this category because the startup costs for the blog were higher in the first year and will cover expenses for the following 3 years.

Automotive ($2,820): 2016 – +$280

Because I drive a lot for work and receive mileage reimbursements that cover gas and wear and tear on my car, I learned this year that I can actually cover all of my automotive costs simply by working. This is especially lucrative since my car is 12 years old and I bought it used, therefore it has already depreciated significantly. This year I ended up making money in this category.

Objects (Take It As It Comes [TIAIC]): 2016 – $1,370

This category includes things like personal care, household items, clothing, gadgets and gear. I decided that rather than determining set budgets for these categories, I would “take it as it comes” and see what my typical spending was. I found that I spent more than I would have liked on household items and unnecessary clothing. But I was happy with the amounts I spent on gear (mainly hiking/camping stuff) and gadgets (phone upgrade and fitbit). These amounts informed my 2017 spending plan allocations.

Misc (TIAIC): 2016 – $420

The miscellaneous category includes things like health, credit card rewards, donations, gifts, and work expenses. Similar to the objects category, I wanted to see how my expenses panned out, and “take it as it comes.” Overall, I spent reasonably in all categories, except for spending too much on gifts.

Losses (TIAIC): 2016 – $205

This category includes things like loans that weren’t paid back and money I’ve spent but did not track where it went (I call this “slush”). Typically slush only happens with cash transactions that I don’t get a receipt for. I do hope to keep this category lower next year than it was this year.

Total Expenses ($6,180): 2016 – $4,485

Total Expenses + Student Loans ($37,125): 2016 – $37,830

Stats

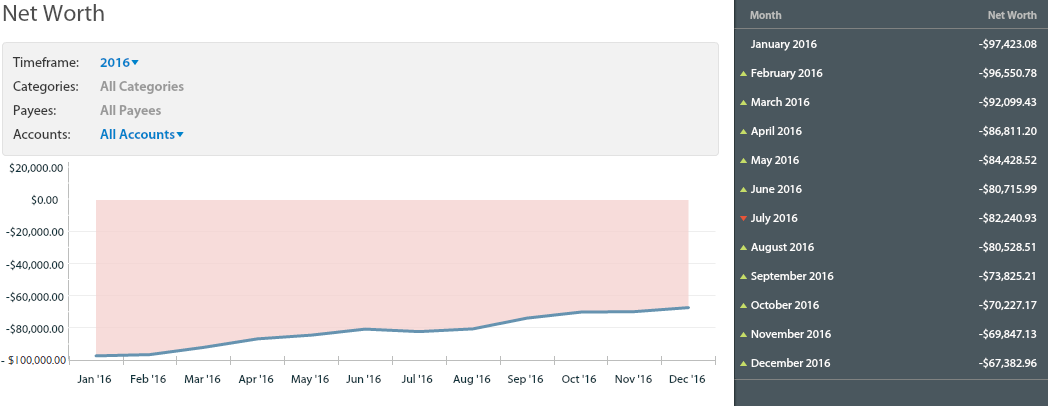

Net Worth

September 2015: -$102,800

January 2016: -$97,400

December 2016: -$67,400

Change in 2016: +$30,000

Change from 2015: +35,400

*This does not take into account my 401k.

Extra Income

Part-Time Income: $450

Additional Full-Time Income: $295

Credit Card and Credit Union Rewards: $240

Misc: $230

Misc included gifts, selling items at a garage sale, and reading the fine print on a “complimentary” magazine subscription – that they would give me money instead of the magazines if I mailed something in.

Interest: $35

Total extra income = $1,250

Investments

401k: Continued contributing to my employer 401k enough to get the employer match.

Insights for next year

- Automate your student loan minimum payments and savings – you won’t feel the money leaving because it is already gone. It never hits your checking account in the first place so you never feel like it’s money you could have spent.

- Earmark your savings. Give them their own account, and give each account a specific purpose. This will fuel your dreams and inspire you to save even more.

- Be flexible. Be willing to frequently re-evaluate your spending plan, your allocations to savings and student loans, and what activities you are spending your time on.

- It is possible to live it up on less than $5,000 per year!

- Get a rewards credit card! This is the easiest money you will ever make.

WANT TO REMEMBER THIS? SHARE THESE TIPS TO PAY OFF STUDENT LOANS TO YOUR FAVORITE PINTEREST PERSONAL FINANCE BOARD!

[…] 2017 Spending Plan is based off of both my 2016 Spending Plan and my actual 2016 spending + some educated guesses about additional expenditures due to changes in circumstances or new […]

[…] 2016 Review – Paying off $33k in Student Loans […]