This article will dive into the following topics:

- Changing Times: Why “good” debt has become a myth

- Bad advice: The outdated advice you hear all the time to avoid at all costs

- Debt alternatives: Options you can consider instead of accruing more debt

- Become debt free: The order in which you should pay off your existing debts

Are you stressed out by your finances because of debt such as student loans, car payments, your mortgage, or credit card debt? You’re not alone. According to a 2017 survey, 54% of workers are stressed about their finances. This is no surprise considering the average American household with debt owes around $135,000! This article will give you some clarity about the types of debt you have, types of debt to avoid, and which types of debt you should eradicate first so you can start to sleep easier at night.

At its core, debt is a financial liability… it’s what you owe to a bank, a credit card, or others.

Here’s the deal – some types of debt are worse than others.

There is No Such Thing as Good Debt

Notice, that I’ll use the term “better” debt, not “good” debt, throughout the article. I think calling a liability “good” is inherently misleading. Some people would disagree, and say that it makes sense to purposely obtain and then leverage your debt to make more money. I disagree with this viewpoint because leveraging debt is risky, and for someone who is interested in pursuing a freedom lifestyle, debt of any kind can seriously delay or diminish your level of freedom.

I also find that this traditional wisdom about leveraging “good” debt comes from older generations, such as Baby Boomers (aka our parents’ generation). However, millennials are more than twice as likely to worry about debt as Baby Boomers, according to a different survey. And although Millennials and Boomers are equally likely to have debt (73% of Millennials and 74% of Boomers), nearly 70% of Millennials have said that debt has negatively impacted their daily life. That’s compared to only 48% of Boomers who feel impacted.

The concept of “good” debt is outdated, misleading, and ultimately financially damaging because Millennials are negatively impacted by debt in a different way than people used to be.

Why Good Debt is Now a Myth

In the modern world, more and more people are seeking the freedom and flexibility of lifestyle design. This concept is particularly popular with Millennials. The currency of this new generation is time and mobility, which means we need to put the old and outdated advice about “good” debt to rest.

Going into debt no longer helps Millennials achieve their dream lifestyles because it restricts the freedom that they seek. Therefore, accruing new debt and “leveraging” it rarely moves younger people towards their goals, because their goals have changed. Before, the goal was to own a nice house and a nice car and keep up with the Joneses. Now, the goal is to have a flexible life with less time spent working and more time spent traveling and gaining new experiences.

Alternatives to Debt

This shift means there has to be a different way to go about things than the old way of leveraging “good” debt. This article is meant to serve as a guide to give alternatives and options that you can consider instead of accruing more debt. I would encourage you to seriously consider what you would be giving up (such as time or flexibility) when you sign a loan or accrue a debt.

Becoming Debt Free

Since 73% of Millennials are already in debt, they also need help navigating the goal of becoming debt free. This article is also a guide to assist you in figuring out which debts you should pay off first. In order to save the most money and reduce your financial stress, it makes sense to address the riskiest and highest interest debts first. Therefore, it is recommended that you pay off debts from Worst to Best as indicated on this list.

The Difference Between Better And Worse Debt

Better debt (again, this isn’t “good” debt) may initially put you in the hole, but the idea is that you will eventually be better off in the long run. This is debt that will help you grow your income (business loans or student loans) or debt that allows you to buy a (hopefully) appreciating asset such as a house. This still isn’t “good” to have because it is risky and can prevent you from living your ideal life. This is debt to avoid having if at all possible, and to focus on paying off after you’ve addressed your worse debts.

Worse debt, on the other hand, is anything the decreases in value the moment after you purchase it. This includes car loans, and credit card debts or payday loans obtained to pay for things like high-end clothes, the latest gadgets, and so much more. This debt costs you a lot of money, and by looking at the numbers you know it’s a bad deal any way you calculate it. This is debt to avoid having at all costs, and the debt you should pay off first if you already have it.

Different Types of Debt, Ranked from Better to Worse

1. Best Debt: Debt From Yourself

Borrowing from yourself is the best type of debt. This isn’t traditionally considered a type of debt. However, it is on this list because not paying yourself back can result in needing to accrue debt from other sources. I’ll admit that this a good kind of debt because you don’t owe anything to an external entity such as a bank. By borrowing from yourself first, you will avoid other, worse types of debt.

This means you have enough money in your savings and emergency fund that you can tap into this pot of money for unexpected expenses or major purchases. But here’s the trick to make it a good debt – after you “borrow” the money from your account (and spend it), set up a monthly payment to the account to replenish the amount you spent. Treat this expenditure as if you had borrowed money from the bank, otherwise, you will just be permanently drawing down your savings or emergency fund.

Make it a goal to pay yourself back with interest too so you will have an even larger cash cushion in the future.

Related Reading:

2. Better Debt: Debt You Can Use to Grow Your Income

Borrowing money so you can grow your income will eventually help you reach your long-term financial goals. However, bear in mind that you are gambling by taking one step backward by shouldering a debt, in the hopes that you can take two steps forward for a better financial future.

These debts include starting a business, buying an investment property, or any other loans that will hopefully grow your future monthly income. A mortgage loan is a good example of this type of debt. The interest rates on them are low (right now) and real estate properties tend to increase in value (appreciate) over the years. In this way, your monthly debt payments, in the right economy, can serve as an investment.

Another example is small business loans. If you want to be rich, your chances are much better if you set up your own company and work for yourself. With the right skill and luck, borrowing money to begin your own business could be the best investment you will ever make.

Have you noticed that a lot of the things that make this a better debt ride on “hopefullys”, the right economy, the right skill and luck, market tendencies, etc? The reason to consider not getting this type of debt, and to consider paying it off if you do have it is because it is inherently a liability. And that makes this type of debt risky to have.

Consider these Alternatives:

- Save for big expenses: Rather than going into debt to purchase a rental property or a primary residence, consider saving your money until you can buy it in cash. This might mean you buy a smaller, less expensive house. This reduces your risk and maintains your freedom. If anything goes wrong in your financial life, you don’t have to worry about your home because you own it outright, so the bank will not repossess it.

- Consider a lower cost option: The same principles apply to starting a business. Business loans can be necessary to start a brick-and-mortar business because of the necessary up-front capital investment, so perhaps consider a different route. Oftentimes for a side-hustle (such as dog-walking, Uber driving, or house sitting) or online business (such as a blog), there is not a large enough up-front cost to require a loan. If there is a small upfront cost associated, you can often pay as you go or save the small amount of money first before launching your business.

- Spend less, make more: Keeping yourself out of debt will enable yourself to make more profits from your business because you won’t be making payments and paying interest on business debt!

3. Better/Worse Debt: Student Loans

Student loans straddle the line between better and worse debt. Student loans are often classified as good debt because they are an investment in your future that can help boost your earning power. However, having sizeable student loan debt can be quite risky.

In fact, one study shows that on average, it will take a university graduate more or less two decades to fully pay off a bachelor’s degree. Additionally, there is virtually no way to gain forgiveness for student loans, even if you declare bankruptcy!

One not-so-bad thing about student loans is that most interest rates are not as high as the interest rates for the bad debt types listed below.

Consider these alternatives:

- If you are thinking about getting your Master’s, get your employer to pay for it, or get a No-Pay MBA

- If you are about to go to college for your bachelor’s, consider the cost as a large factor when selecting a school (I didn’t do this, and I regret it)

- Work a job or two (I had 4 at one time!) while in school to offset your costs and avoid taking loans

Related Reading:

If you already have student loan debt, read these to get some clarity on paying it off quickly to reduce stress and save money on interest:

- How I paid off $67,000 of High Interest Student Loans in Less than 2 Years – and Saved $23,600 in Interest!

- Q2 2017 Financial Review – $21,500 of Student Loans Paid Off

- Q3 2017 Financial Review – $4k of Student Loans Paid Off + $5k Emergency Fund Saved

- 2017 Review – $27k Student Loans Paid Off + $17k Saved

- 2016 Review – Paying off $33k in Student Loans

4. Worse Debt: Automobile Debt

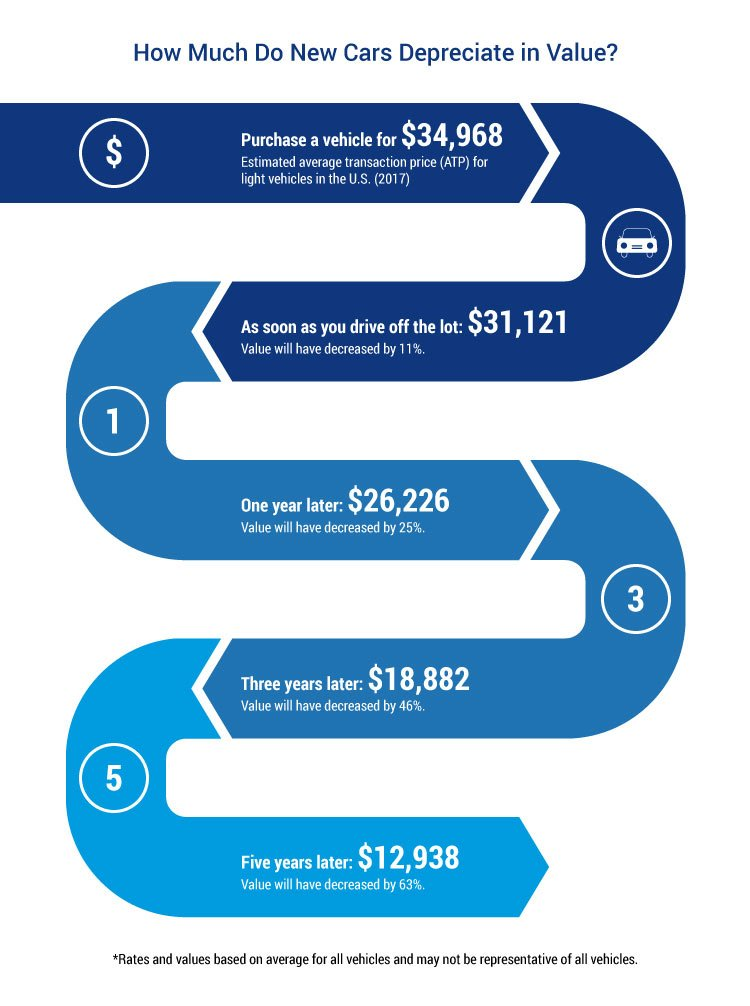

Most of us just can’t afford to simply walk into a car dealership, drop a suitcase filled with cash, and take home a brand new car. However, borrowing money to purchase a depreciating asset is definitely a bad move. A car is a swiftly depreciating asset – a car can lose up to 11% of its value the second you drive it off the lot. 12 months later, the car will have lost 25% of its value, and by 3 years later the car will have lost nearly half (46%) of its value! Those rates of depreciation mean the amount you need to borrow immediately can’t be covered by re-selling the car you have just purchased.

Automobile interest rates can also be quite high, depending on your credit score. If you have a bad credit score, you could be paying over 15% interest for a 5 year loan! Even with a good credit score, you will be paying between 4% and 7% interest, which is too high to pay for a vehicle you are losing money on every month through depreciation. You are already in the red before you have even made the first interest payment, so just say no to automobile debt.

Consider these Alternatives:

- Good – Buy a 1 Year Old Car: Still want a new car, but don’t want the bad debt that comes with it? Consider buying a “barely used” car that is about a year old. Sure, someone may have put a few thousand miles on it, but the warranty will still be good and there might even be a little of the new car smell left. Most importantly, the original purchaser will have suffered the major depreciation, which puts you, the buyer, at an advantage. You will pay 25% less for the car, even though it is practically new. For a $35,000 car (this is the average cost of a new light vehicle in 2018), this means you will be saving $8,750.

- Better – Wait 3 Years to Buy: If you were to wait 3 years to buy the new car you have your eye on, the vehicle would have lost 46% of its value (to the financial dismay of the person who bought it new), which means you will be saving $16,100. The price you pay will now be around $18,900. That means you can spend these three years saving $6,300 per year so you can avoid taking a loan when you go to buy the car. With a 5 year, $35,000 car loan at an average interest rate of 4.21%, you would have been paying $620/month ($7,440/year). If you save that money instead, you will save the full cash payment AND an extra $1,140 each of the 3 years you are collecting money for your cash purchase of the car. Then you will save $7,440 for the following 2 years. That’s a lot of money that can be invested now so you can start putting your money to work for you.

- Best – Buy an Older Car: The final option to consider is to buy an older vehicle (between 4 and 15 years old). This vehicle may be out of warranty, but there are plenty of used cars that are available for under $10,000. Try to strike a balance between the purchase price of the car and the maintenance cost for the car. Older cars will be cheaper up front but may cost more to maintain. Ask yourself if the stress of having debt to have a newer car is worth it to you. Then consider the things you could use $25,000 for, such as investing or paying off other debt (which will increase your overall cash flow).

- Real Life Example: I bought my car about 7 years ago (it is now about 15 years old) for $6,500 cash (yes, I saved my butt off to put together that amount of money in college). If I put $3,500 into it for maintenance, that’s a total $10,000 investment for 7 years. That means this car has cost me $1,430 per year, or just under 1/5 of what that average car payment would have cost. And I have never paid a penny in interest, or worried about whether I could afford a payment in a given month.

5. Worst Debt: Credit Card Debt

Credit cards are great – if you pay them off in full every month. They can help you track your spending, earn cash back or travel rewards, and are easier than shuffling through a pile of bills at the cash register. However, carrying a balance on your credit card – AKA credit card debt – is one of the worst types of debt you can have.

The average credit card interest rate right now is between 13% and 19%. Some introductory interest rates can start at 0%, or the low end of the average range, and quickly balloon to over 25%.

If you are carrying a balance, it can get expensive fast. For an instance, if you have charged $3,000 to your card but you can only afford to pay $100 at the end of the month, it will take you three years to pay back, not including the sky-high interest. And at 19% interest, this purchase will have cost you almost $1,000 more in just interest!

Consider this:

- Pay off credit card debt first: If you are looking at your different types of debt and are not sure which ones to tackle first, credit card debt is usually a good first choice. That’s because the interest rates are typically the highest, so by paying off this debt, you are freeing up significant cash flow that can then be used to pay off your remaining debts. You’re also saving the most money by tackling this first.

- The above is the Avalanche Method, where you pay off debts with the highest interest rate first.

- If you have debts with the same or similar interest rates, consider using the Snowball Method, where you pay off the smallest balances first to gain some quick wins.

- Save an emergency fund: Having an emergency fund can keep you from accruing credit card debt in an emergency. Read #1 Borrowing from Yourself for related readings about emergency funds.

- Devise a method to avoid future CC debt: Find a method that works for you – maybe it’s cutting up all your cards, or freezing them in a block of ice, or a shopping ban, or using the envelope system. Whatever works, just make sure you’re not adding to the credit card balances that you’re trying to pay off!

6. Definitely the Absolute Worst Debt: Payday Loan

A payday loan is a quick cash loan, but unlike credit card debt, this type of debt has relatively minimal qualification requirements and almost zero waiting time. It’s possible, and in fact very convenient, for you to take out a small short-term cash loan with a superbly low promotional rate at any payday loan shop you can find near you.

However, the downside of these incredible promotional rates is that they don’t last long. In fact, it can come with unusual fees and annual interest rates that usually go beyond 400%. This means that a payday loan can balloon much faster compared to other types of debt. If you can’t immediately repay your payday loans, you will find yourself in an interest-building nightmare.

This is the worst type of debt on the list, but it’s also the most unusual type. If you are reading personal finance blogs, you might not have even known about this type of debt. I still thought it was good to mention so you can avoid this debt at all costs in the future.

Consider these Alternatives:

If you’re considering a payday loan, you may be in bad financial straits right now. Since this is the absolute worst type of debt ever (not exaggerating!), I would recommend considering different types of “better” debt before going the route of the payday loan. First, however, try to make more money so that the loan is unnecessary, or at least you can borrow a smaller amount of money.

- Earn more money: Get a side gig, sell your stuff, rent a room in your house. Desperate times call for desperate measures, and working longer hours is better than going into debt.

- Borrow against your 401k or IRA: There are significant penalties for this if it’s not done properly, but it’s better than a payday loan. Research and talk to a professional.

- Take out a home equity line of credit: If you own a home, you can borrow against the equity you’ve put into it (your downpayment and mortgage payments). This is not advisable if it can be avoided since you are just increasing your mortgage debt. However, this type of debt tends to have favorable interest rates.

- Get a personal loan: Take a personal loan and make a solid plan to pay it back quickly.

- Ask a friend or family member: Borrowing money from friends or family isn’t advisable, and could strain your relationship with that person. If you can’t get approved for a personal loan, this may be something to consider. Do offer to pay interest on what you borrow, and create a payment plan that you take seriously. However stressful this might be for your relationship, it is still better than a payday loan or owing a loan shark who will break your legs if you don’t pay, just sayin’.

- Use a credit card: Same as getting a personal loan – you have to make a plan to pay it back quickly. This is only listed below asking friends or family because the interest rates will likely be higher. However, depending on your situation, you may want to consider credit cards before personal relationships.

Living Debt Free

Living debt free can seem like an unusual, if not impossible, way of life for many people. The traditional necessities of the past – houses and cars – often seem to “require” debt based on their high price tags. Therefore, it’s no surprise that there is an outdated concept of “good” debt that helps you get ahead in life.

The worst debt is definitely any debt that you can’t pay, especially ones with a higher interest rate. But in the modern world where time and mobility are the new currencies and Millennials want more out of life than just a 9 to 5 and a house and a car, “good” debt has become a myth. All debt is bad – there is only better debt and worse debt. Debt that is acceptable but risky, and debt that has to be paid off as quickly as possible at all costs.

This ranking of debt from better to worse should help you figure out what debts you might want to pay off first to reduce your stress and save the most money. Also, use this as a guide when considering whether to get into debt for certain types of purchases in the first place. Remember, debt is a financial responsibility that will restrict your freedom and can ultimately limit your ability to live your ideal life for years to come. Keep that in mind before borrowing!

Your Turn:

What debt will you pay off first? Share your plan with me in the comment section below. I would love to hear from you.

WANT TO REMEMBER THIS? SAVE THESE TIPS TO YOUR FAVORITE DEBT PINTEREST BOARD!

[…] making bad financial decisions. For example you might consider accruing debt (and there’s no such thing as good debt) to cover an emergency. But you won’t have to resort to credit cards or loans if you have an […]

[…] Sources for most statistics can be found in this article […]

[…] Millenials in Debt: Ignore Outdated Advice and Become Debt Free […]