Q2 was a great quarter — I put over $21,000 towards shrinking my $100,000 high mountain of debt! That’s over 20% of the total I owed when I graduated college. Quarter 2 (April, May, June) is where I try to learn from my Q1 Spending Plan Review and address my problem spending areas. I tried and succeeded at learning from my mistakes, and ended up going above and beyond in making up my missed Q1 extra student loan payments.

The biggest takeaway from Q2? Shit happens. And it all shakes out in the end – don’t get discouraged when something unexpected takes you off track, just become determined to get yourself back on track. I put my mind to making up my student loan extra payments that got screwed up last quarter, and I ended up exceeding my plan by thousands of dollars!

Spending Plan Review

(April, May, June 2017)

The first number shown is the yearly allocation for the category, and the Q2 – $ amount shows how much was spent in Quarter 2 – April through June. In parentheses, the percentage spent of the yearly allocation is shown.

(Read this post for an introduction to spending plans)

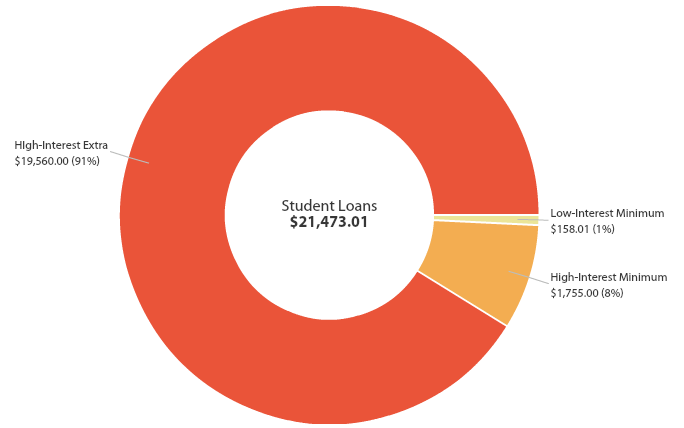

Student Loans

Low-Interest Minimum Payment – $790: Q2 – $160 (20%)

High-Interest Minimum Payment – $7,025: Q2 – $1,755 (25%)

High-Interest Extra Payment – $24,000: Q2 – $19,560 (82%)

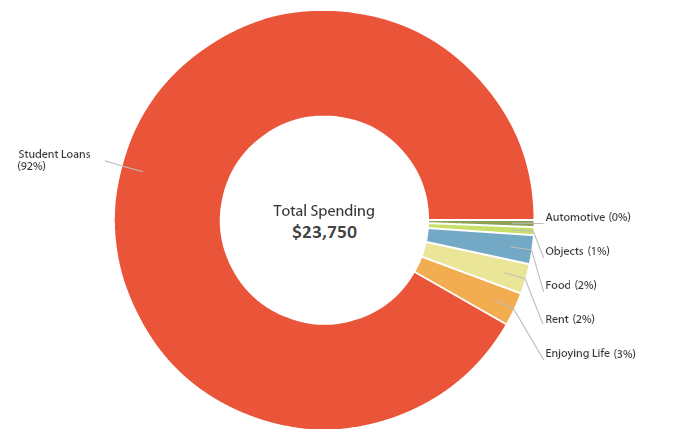

Halfway through the year I’ve already hit 67% of my payment goal for my student loans! Of course, the $19,500 that went towards my extra payment on my high interest loans was supplemented by money I had saved last quarter and was unable to put towards my loans due to technical issues at the time. This aggressive payment of my high interest student loans enabled me to pay off $68,000 of my student loans in less than 2 years. 92% of my spending was on paying off my debt, therefore increasing my net worth and my freedom. Each other spending plan category was individually under 3% of my spending for the quarter.

Student Loan Payments – $31,815: Q2 – $21,475 (67%)

Savings Goals

Savings Goals: Q2 – $0 (0%)

Just like last quarter, my savings goals are on hold while I divert all “extra” money towards my high-interest loans. All money previously saved was diverted to the student loans, and currently savings are frozen for the first approximately three-quarters of the year. I have a $500 emergency fund and several thousand dollars in the bank each month. Saving is scheduled to resume in September 2017, with a $10k emergency fund goal by the end of the year.

Total Savings – $0: Q2 – $0

Expenses

Enjoying Life – $2325: Q2 – $615 (27%)

It makes me feel good when I’m close to my spending goal and also manage to achieve so many things on my to-do list! This quarter I stopped going to boxing classes and bought some inexpensive boxing mitts instead, so I can train at home (outside!) for free with my partner. I obtained two different licenses this quarter – motorcycle and boat. With the license came expensive motorcycle gear- which is something to watch out for. Have you ever noticed that spending begets more spending? At this point, I’ve exceeded my 2017 Motorcycle allocation by $135. I am determined to not spend any more on my motorcycle this year. Additionally, weddings, concerts, camping, and kayaking were all on the experiential list this quarter. Overall, I would consider this category a win, considering how many great experiences I had for an average of $205 per month.

Food & Alcohol – $2,220: Q2 – $635 (29%)

Like last quarter, I overspent quite a lot on alcohol and dining. Weddings and a family emergency that involved almost a week in the hospital (read: buying expensive convenience food in order to stay nearby) jacked up the dining bill. Rehearsal dinners and going away parties contributed to the high expenditures on alcohol. Groceries came in extremely under budget due to moving back in with family briefly due to the aforementioned medical emergency. And I didn’t spend any money at all on junk food (self-five!). I still over-spent in this category even though grocery expenses were minimized. I will work harder to decrease my spending on food and alcohol next quarter.

Business – $225: No spending in this category in Q2 (0%)

Automotive – $2,930: Q2 – $60 (2%)

At $60 for three months of automotive costs, color me thrilled. Again, this is all thanks to reimbursements for work-related travel – my fuel/maintenance cost for the quarter actually came out positive! Driving the beater I do, rocking over 176k miles, is actually making me more and more money the longer I continue to drive it. It helps me get over the fact that the paint job is fading and chipping terribly and it’s 13 years old. Tolls came out to a whopping $94 and I paid an additional $55 towards my car insurance, the bulk of which I paid last quarter. Can’t complain about that.

Rent – $1,200: Q2 – $380 (32%)

As I mentioned last quarter, I pay my rent in home improvement investment and labor. Since it was spring and summer, we started our backyard project and the materials were relatively costly. But to have a new, gorgeous raised bed organic garden that we built with our own hands is totally worth it. I’ll be reaping the benefits in the form of fresh salads for the rest of the year.

Objects – $1,010: Q2 – $145 (14%)

Despite a bit of a home décor shopping spree ($50), and buying some clothes at a garage sale that didn’t really fit and I never needed in the first place, I did well in this category this quarter. I bought some stuff that I let sit in my Amazon shopping cart for 3 months to make sure that I still needed it – and turns out I didn’t need everything, so I only bought the necessities ($52). Due to Q1 spending, I am over my annual spending goal for clothing, and I’m at about 75% of my goal for non-consumable household items. Otherwise, I’m feeling confident about this spending category – halfway through the year I have not spent money on gadgets or gear at all, and year-to-date I’m at 35% of my goal at 50% through the year.

Misc – TIAIC: Q2 – $435

Most expenditures were on gifts – multiple weddings, housewarming parties, and of course Mother’s Day put me over my annual allocation (113% spent at this point). Thank goodness I already bought all of my Christmas presents in Quarter 1! I had a few more extraneous healthcare costs.

Losses – TIAIC: Q2 – $5

Cha-ching! It looks like I managed to keep a close eye on my cash expenditures this quarter, with under $10 spent on who-knows-what.

Total Expenses – $10,165: Q2 – $2,275 (22%)

Total Expenses + Student Loans – $41,980: Q2 – $23,750 (57%)

Extra Income

Additional Full-Time Income: $830 – The additional income I received is net income from working overtime.

Credit Card and Bank Rewards: $95 – All credit card cashback bonuses, which I applied directly to my bill, freeing up extra money to put towards my student loans.

Interest: $2

Part-Time Income: $0 – I was furloughed for this portion of the year, since my job was outside and the weather was not conducive to performing it.

Total Extra Income = $927

Investments

401k: Continued contributing to my employer 401k enough to get the employer match. When I make additional income at my full-time job, my 401k contribution (which is a percentage) increases and so does the employer match!

Final Thoughts

I am feeling very confident after this quarter. I believe that I will not only meet, but I will exceed my financial goals this year, based on the numbers so far. Though I overspent in a few areas, overall, my spending followed my Spending Plan closely. Beyond that, I absolutely crushed my goals with regards to paying off my student loans. I spent an average of under $800 a month for all expenses besides my loans, and an average of nearly $8,000 each month towards my loans!

WANT TO REMEMBER THIS? SHARE THESE TIPS TO PAY OFF STUDENT LOANS TO YOUR FAVORITE PINTEREST PERSONAL FINANCE BOARD!

[…] Q2 2017 Financial Review – $21,500 of Student Loans Paid Off […]